Ticket to Ride or Ticket to Nowhere? Debating NOW

Sarah Chen (Bull):

Alright, the stock's down 10% after hours and I know you're sharpening your knives, Marcus. But before you start dancing on what you think is a grave, let me explain why this is a gift.

For anyone who needs the refresher: ServiceNow is the plumbing of the modern enterprise. They started in IT service management — basically, when your laptop breaks and you submit a ticket, that ticket lives in ServiceNow. But over the past decade they've expanded into HR workflows, customer service, security operations, risk management, and now they're positioning themselves as the orchestration layer for enterprise AI. When a company wants to deploy AI agents across their business, ServiceNow is betting they'll need a platform to govern those agents, connect them to data, and make sure they don't go rogue. That's the pitch.

Now, the quarter. Let's be honest about what actually happened here. Subscription revenue grew 21% year-over-year. cRPO — which is basically contracted revenue coming in over the next twelve months — grew 22% in constant currency. Operating margin was 29.5%, 50 basis points above guidance. They beat on every metric they guided to. Bill McDermott came out and said they "exceeded expectations on top of a beat and raise track record." This is a $200 billion market cap company growing subscription revenue north of 20%. Find me another one.

So why is the stock down 10%? Two reasons, and neither of them are structural.

First, 2025 guidance came in at 19.5-20% subscription revenue growth versus whisper numbers closer to 21%. That's a $175 million FX headwind they called out explicitly. The dollar ripped. That's not a demand problem, that's a currency translation problem.

Second, cRPO for Q4 came in at $10.27 billion — slightly below the $10.43 billion some analysts had penciled in. But again, they called out $205 million of incremental FX headwind since September. Back that out and they beat.

Here's what the market is missing: 150% quarter-over-quarter growth in Pro Plus AI deal count. Now Assist — their GenAI add-on — is getting pulled into deals at an accelerating rate. McDermott said the agentic AI shift is "the seismic opportunity of our time" and that ServiceNow is positioned as "the AI control tower for business transformation." This isn't hype — they've got 500 customers north of $5 million ACV, up 21% year-over-year. These are enterprise behemoths betting their digital transformation on ServiceNow.

At 45x forward earnings for a company growing 20%+ with 30% operating margins and accelerating AI monetization? This sell-off is a buying opportunity. I'm adding.

Marcus Webb (Bear):

Sarah's doing what ServiceNow bulls always do: explaining why the miss doesn't matter and why the guidance is actually good if you squint hard enough. I've heard this song before.

Let me start with the numbers. Yes, they beat on Q4 metrics. Congratulations on clearing a bar you set yourself. But the forward guidance is what matters, and here's what the market actually heard: 2025 subscription revenue growth of 19.5-20%, down from 21% in 2024. cRPO growth guided to 20.5% for Q1, which is a deceleration. And they're introducing consumption-based pricing for agentic AI, which means less predictable revenue recognition going forward.

Sarah wants to blame FX. Fine, currencies moved against them. But you know what else moved? The entire AI landscape. DeepSeek just dropped a model that performs comparably to GPT-4 at a fraction of the cost. Compute costs are collapsing. Every software company that was planning to charge $50 per seat for AI features is now staring at a world where the underlying models are becoming commoditized.

And here's my real concern: what exactly is ServiceNow's moat in an agentic AI world?

Let me explain what I mean. ServiceNow's core business is workflow automation. You submit a ticket, it routes to the right person, they resolve it, the ticket closes. Very useful. Very sticky. But agentic AI — the thing McDermott keeps hyping — is about AI systems that can autonomously take actions. If an AI agent can diagnose and resolve IT issues without human intervention, what happens to all those ServiceNow seats? If an AI can automatically triage customer service requests and solve 80% of them, do you need as many customer service agents using ServiceNow?

McDermott says "it doesn't matter who builds the models" and that ServiceNow sits at the "business impact layer." That's a nice narrative. But the business impact layer is exactly where AI disruption hits hardest. If the models get cheap and capable enough, the orchestration layer starts looking like middleware that can be rebuilt by anyone with access to the same APIs.

KeyBanc downgraded the stock in December specifically citing AI disruption risk and "seat count pressure." They're not wrong to be worried.

The stock is down 10% and still trades at 45x forward earnings for decelerating growth. That's not a buying opportunity. That's the market starting to ask hard questions about whether the next decade looks like the last one.

ROUND 1: THE AI DISRUPTION QUESTION

Sarah Chen:

Okay, let's address the AI bear case directly because I think it's fundamentally misunderstood.

Yes, LLM costs are dropping. Yes, DeepSeek is impressive. But here's what Marcus is missing: falling AI costs are good for ServiceNow, not bad.

McDermott said it explicitly on the call — and I'm paraphrasing here — "with the precipitous drop in LLM compute costs, there is much more capital allocation available for the business impact layer." Translation: enterprises have finite AI budgets. If they're spending less on raw compute, they have more to spend on the orchestration and workflow layer. That's ServiceNow's sweet spot.

And on the "AI will eat seats" argument — this is the same thing people said about RPA five years ago. Robotic process automation was supposed to eliminate the need for half the back-office workforce. What actually happened? Companies automated tasks, productivity went up, and they redeployed humans to higher-value work. Net effect on ServiceNow seats? Zero to positive.

Agentic AI is the same story. Yes, AI agents will resolve more tickets autonomously. But someone has to build those agents. Someone has to govern them. Someone has to audit what they're doing and make sure they don't create security vulnerabilities or compliance violations. That's where ServiceNow's AI Control Tower comes in. They're not selling seats to humans doing repetitive work — they're selling the governance layer for AI doing work autonomously.

And by the way, they just announced they're acquiring Armis for cybersecurity. Why? Because as you deploy more AI agents across your enterprise, your attack surface expands. You need security tooling that understands the AI stack. ServiceNow is positioning themselves to own both the workflow and the security layer. That's called strategic thinking.

Marcus Webb:

Sarah's making the classic bull case error: assuming that because ServiceNow's management says they're positioned for AI, they actually are.

Let me give you a concrete example of why I'm skeptical. Just this month, a security researcher found what he called "the most severe AI-driven vulnerability to date" in ServiceNow's platform. A flaw in their Virtual Agent API combined with their Now Assist agentic AI allowed an unauthenticated attacker to impersonate any user in the system using just an email address. No MFA bypass needed — the system just trusted whoever claimed to be the user. The researcher was able to create himself an admin account with full privileges.

Now, ServiceNow patched it quickly, credit to them. But this is exactly the kind of thing that happens when you bolt AI onto legacy systems. ServiceNow's Virtual Agent is basically a chatbot they built years ago. Now they're layering agentic AI on top of it, giving those agents the ability to take privileged actions across the enterprise, and the security architecture wasn't built for that.

This isn't a one-off. There was another report in November about prompt injection vulnerabilities where ServiceNow AI agents could be tricked into acting against each other. The response from ServiceNow? "The system works as intended."

My point isn't that ServiceNow can't fix these issues. My point is that the transition to agentic AI is hard, it's risky, and it's not obvious that the incumbent workflow player wins. Salesforce is building Agentforce and just added 6,000 customers in a single quarter. Microsoft has Copilot deeply integrated into the stack every enterprise already uses. Google and Anthropic are both pushing agentic capabilities.

ServiceNow is betting that enterprises will choose them as the "control tower" for AI governance. But that's a new market, not their existing market. And in new markets, incumbency doesn't guarantee victory.

ROUND 2: MANAGEMENT COMMENTARY AND STRATEGY

Sarah Chen:

Let's talk about what McDermott actually said on the call, because I think it's important.

When asked about DeepSeek, he didn't panic. He said — and this is close to a direct quote — "It doesn't matter to ServiceNow who builds the models. With the precipitous drop in LLM compute costs, there is much more capital allocation available for the business impact layer. Our position at the center of data, AI agents, workflow orchestration, and enterprise governance is the nexus of AI's massive value creation opportunity."

That's not a CEO dodging the question. That's a CEO who's thought through the implications and has a coherent strategy. ServiceNow isn't trying to compete with OpenAI or Anthropic or DeepSeek on building foundation models. They're trying to be the layer that enterprises use to deploy, govern, and orchestrate whatever models they choose.

And the numbers support the strategy working. Pro Plus AI deals — their premium AI offering — grew 150% quarter-over-quarter. Workflow Data Fabric, which is their data integration layer, was in 16 of the top 20 deals. RaptorDB Pro, their high-performance database, more than tripled net new ACV year-over-year. These aren't vaporware announcements — they're products shipping and generating revenue.

Gina Mastantuono specifically called out that they're giving away agentic AI capabilities inside existing Now Assist subscriptions rather than charging separately. Why? Because they want adoption first, monetization second. Once an enterprise has ServiceNow agents running across their IT, HR, and customer service workflows, they're not ripping that out. The switching costs are enormous.

This is the classic land-and-expand playbook that's made ServiceNow a compounding machine for fifteen years. I trust them to execute it again.

Marcus Webb:

Sarah trusts management. I trust the numbers.

Here's what the numbers say: subscription revenue growth is decelerating. It was 27% in Q4 2023, 25.5% in Q1 2024, and now 21% in Q4 2024. Guidance for 2025 is 19.5-20%. That's a clear downward trajectory, and management is explaining it away with FX headwinds and "strategic investments in adoption."

On the AI monetization point — yes, they're giving away agentic capabilities to drive adoption. But that's a bet that eventually these capabilities will drive incremental revenue through token consumption. Gina said "the extra token monetization has not been significant" so far. They're hoping it will be. Hope is not a strategy.

And the consumption model introduces new uncertainty. Traditional SaaS is beautiful because it's predictable — you know what customers owe you each quarter. Consumption-based pricing means revenue depends on how much customers actually use the product. If agentic AI underdelivers on productivity gains, usage won't ramp. If competitors offer better agents, customers use those instead.

Here's the other thing that bothers me about McDermott's commentary: he keeps talking about ServiceNow as "the defining enterprise software company of the 21st century" and targeting $30 billion in revenue "and beyond." This is a company doing $11 billion in revenue today. To get to $30 billion, they need to nearly triple. At 20% growth, that takes about six years of perfect execution.

But software multiples are compressing. Interest rates are higher than the ZIRP era. And AI is genuinely disrupting how enterprises think about software spending. The assumption that ServiceNow can sustain 20% growth for six more years, in a world where AI agents might fundamentally change the need for workflow seats, seems optimistic.

I'm not saying ServiceNow is a bad business. I'm saying it's priced for perfection in an increasingly uncertain environment. When you're at 45x earnings, you don't have room for error. The 10% drop today is the market realizing that.

ROUND 3: VALUATION AND RISK-REWARD

Sarah Chen:

Let's talk valuation, because I think this is where the setup gets interesting.

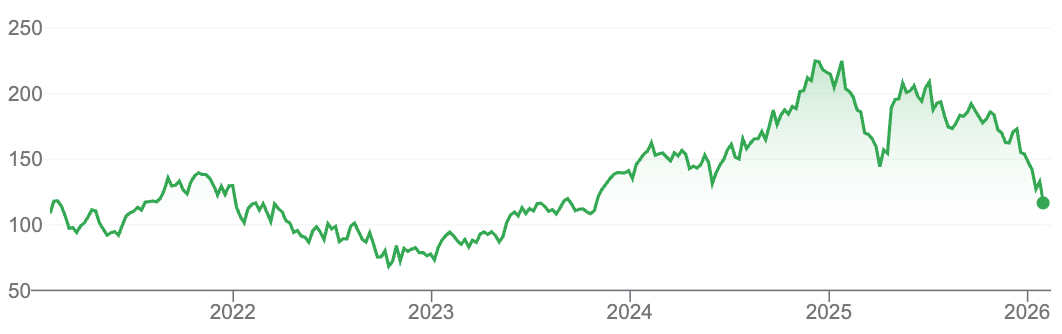

Pre-earnings, ServiceNow was trading around $1,15. Now it's at $1,03. On a forward P/E basis, that's roughly 45x 2025 earnings. Expensive? Sure, on an absolute basis. But let me put that in context.

ServiceNow is one of maybe five large-cap software companies still growing 20%+ at scale. They have 98% renewal rates. Gross margins are north of 80%. Free cash flow margin hit 47.5% in Q4. They have $10 billion in cash on the balance sheet. The business generates enormous amounts of cash while still investing heavily in AI.

Compare that to the other large-cap software names. Salesforce is growing mid-single digits and trades at 26x. Adobe is growing low teens and trades at 24x. SAP is growing 10% and trades at 30x. ServiceNow is growing 20% with better margins than all of them and trades at a premium that reflects that.

And here's the thing about premium valuations: they persist when the underlying business keeps executing. ServiceNow has beaten expectations for something like 50 consecutive quarters. The one quarter where guidance comes in light on an FX headwind, and the stock gets whacked 10%? That's called an opportunity.

If they execute on AI monetization over the next 12-18 months — and the Pro Plus deal growth suggests they will — you're looking at a re-rating, not de-rating. I'll take my chances at $1,030.

Marcus Webb:

Sarah's comparing ServiceNow to Salesforce and Adobe as if those are the only alternatives. The real comparison is to the market's expectations embedded in the stock price.

At 45x forward earnings, ServiceNow needs to grow EPS at 15%+ annually for the next decade just to earn a market return from here. That's not impossible, but it requires sustained excellence in an environment where AI could change the competitive dynamics entirely.

Let me paint the bear scenario. AI agents get good enough that enterprises need fewer workflow seats — not tomorrow, but over 3-5 years. ServiceNow's renewal rates start to dip from 98% to 95% as customers consolidate licenses. Growth decelerates from 20% to 15% to 12%. The stock re-rates from 45x to 30x, which is still a premium multiple.

In that scenario, you're looking at a stock that goes from $1,030 to $750 over three years. That's a 25% drawdown in what's supposed to be a "quality compounder."

Now, maybe that doesn't happen. Maybe agentic AI is additive to ServiceNow's TAM rather than cannibalistic. Maybe they successfully become the AI Control Tower and expand their footprint. But that's a lot of "maybes" for a stock priced for certainty.

I'd rather wait for a better entry. If ServiceNow prints 20%+ growth for another two quarters and AI monetization starts showing up in the numbers, I'll pay a higher price with more conviction. But paying $1,030 today for a stock that just guided to decelerating growth and has a major strategic question mark hanging over it? That's not my trade.

CLOSING STATEMENTS

Marcus Webb:

Look, I want to be clear about something. ServiceNow is a great business. Bill McDermott is a great operator. The platform is genuinely valuable to enterprises and the switching costs are real. I'm not saying this is a short.

But "great business" and "great stock" aren't the same thing at 45x earnings.

The quarter was fine. Not great, not terrible. They beat on the metrics they guided to and then guided to slower growth next year. The AI narrative is compelling, but it's narrative — the actual AI revenue contribution is still "not significant" by their own admission. And the competitive landscape is shifting fast.

In the meantime, they announced a $3 billion buyback, which tells you management thinks the stock is undervalued. Maybe they're right. But I've seen enough high-multiple software companies announce buybacks right before a prolonged derating to be skeptical.

ServiceNow might be the AI platform winner. Or they might be the 2010s workflow winner that gets disrupted by the next wave. At these valuations, you're paying for the former and ignoring the possibility of the latter. That's not how I invest.

Sarah Chen:

Marcus makes a reasonable bear case, and I respect that he's not throwing around "ServiceNow is dead" takes like some of the Twitter geniuses tonight.

But here's where I disagree fundamentally: he's treating AI as a risk to ServiceNow when I think it's the catalyst that extends their growth runway.

The old ServiceNow story was "we help enterprises automate IT and HR workflows." The new story is "we're the governance and orchestration layer for enterprise AI." That's a bigger TAM, not a smaller one. And they're not pivoting from scratch — they have 8,000 customers, including 85% of the Fortune 500, already running mission-critical workflows on their platform. Those customers aren't going to Microsoft or Salesforce for AI governance. They're going to whoever already knows their data, their processes, and their compliance requirements. That's ServiceNow.

On the valuation point — yes, 45x is premium. But premium multiples compound when growth persists. Look at what happened to investors who said Amazon was too expensive at 50x, or Nvidia at 40x, or Microsoft at 30x. At some point you have to pay up for quality.

Is there execution risk? Of course. Is there a scenario where AI disruption hurts them? Sure. But at $103 after a 10% drawdown on an FX-driven guidance miss, I like the risk-reward.

The world works with ServiceNow. I'm betting it still will in five years.

Marcus Webb:

For the record, I didn't say Amazon or Nvidia. I said ServiceNow at 45x in a decelerating growth environment with AI uncertainty. Subtle difference.

End of Transcript

Key Points Summary

| Factor | Bull Case (Chen) | Bear Case (Webb) |

|---|---|---|

| Q4 Results | Beat on all guided metrics; 21% subscription growth at scale | Slight cRPO miss; growth decelerating from 27% to 21% |

| 2025 Guidance | 20% growth despite $175M FX headwind; underlying demand strong | 19.5-20% guidance vs 21%+ whispers; deceleration trend |

| AI Impact | Falling LLM costs benefit orchestration layer; 150% Pro Plus deal growth | Commoditizing models threaten seat count; competitors building fast |

| Management Strategy | Land-and-expand with AI; adoption first, monetization follows | Consumption-based pricing introduces uncertainty; AI revenue "not significant" |

| Valuation | 45x for 20% grower with 80%+ margins; premium justified | Priced for perfection; no room for error; re-rating risk |

| AI Security | Patched quickly; normal growing pains | "Most severe AI vulnerability to date" exposed architectural risks |

Disclaimer: This is a fictional debate for educational purposes. The views expressed do not represent actual investment advice or real individuals.